A California driver explains their family's experience,

“We found that the legacy insurance companies were considerably more expensive than other options for insuring our Tesla. We switched from a legacy company to Costco for our insurance, and we only pay $800 per year to insure our Model Y with great coverage. Tesla itself offered similarly-priced insurance, but we’re not totally convinced it’s the right decision over a more neutral third party.”

2025 data from Insurify, an insurance data aggregator, shows the average price of EV insurance is 49% higher than insurance for an equivalent gas car. But, this data is based on comparisons to gas cars that have, on average, a 50% lower purchase price. For instance, this data compared the Honda Prologue, with an average MSRP of $53K, to the Honda CR-V, with an average MSRP of $30K.

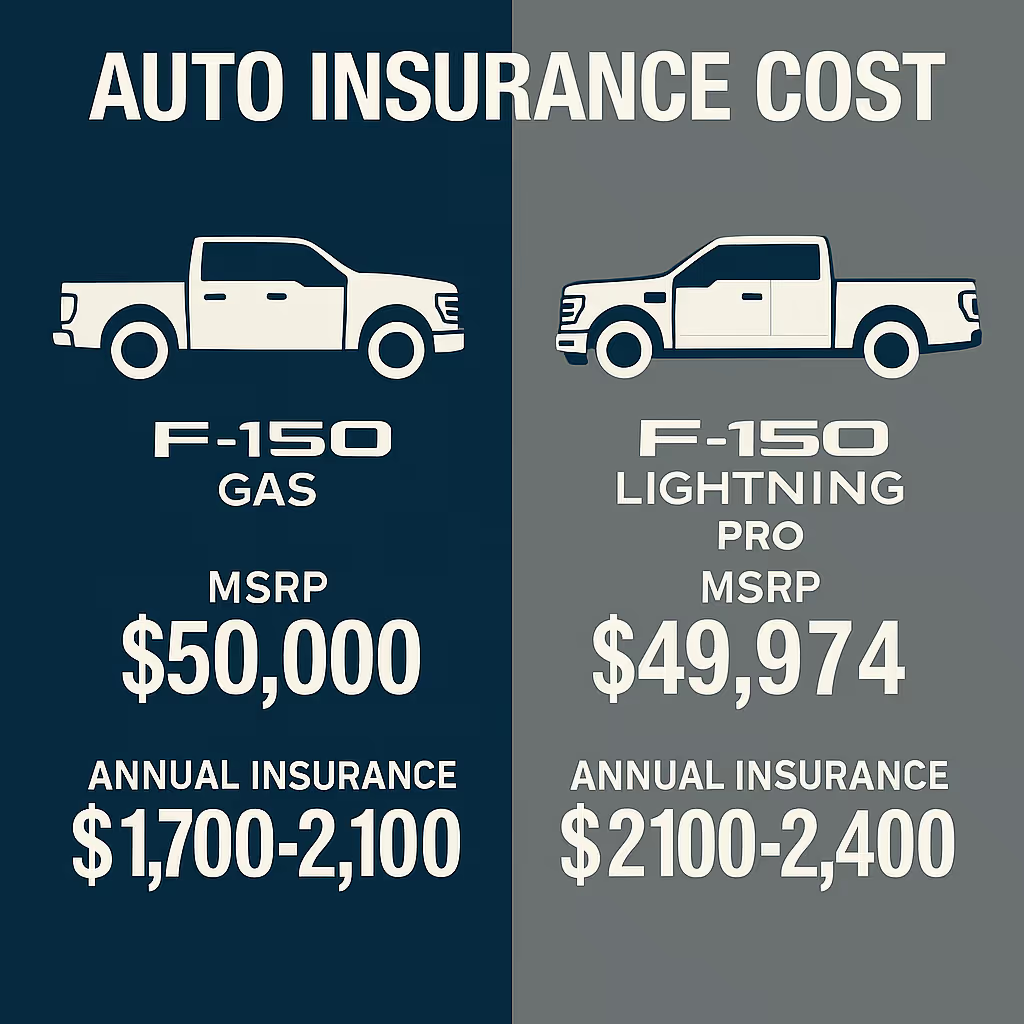

Since insurance costs are tied to the price of the car, this comparison may not be perfect. When you look at comparably priced cars, such as specific versions of the gas and electric Ford F-150, EVs are, on average, still slightly more expensive to insure.

One thing that's certain, is that different insurance providers have very different EV offers.

Shop Around to Save

Despite the data, many savvy EV drivers have shopped around to find competitive rates to insure their EVs. However, there is no single company that will save you money. It depends on your location, your car, and any available bundles or incentives.

A family in North Carolina switched from USAA to Progressive when they traded in their 2023 Subaru Crosstrek - valued at $18-$20K for trade in, for a 2023 Kia EV6 Wind Long Range, valued at $23,400 at purchase.

USAA's price to insure the Kia EV6 was $50 more per month than to insure the Subaru, whereas Progressive actually saved them $10/month.

Every other quote from every major car insurance company was more than USAA or about equal. Some were outrageously more, like AAA’s partner insurance program.

Meanwhile, for a family in Iowa, State Farm insurance for their Rivian was half the price of Nationwide, Progressive and Geico. A rep mentioned that it was due to how State Farm calculated the values for EVs.

Why EVs Cost More to Insure - For Now

There are several factors contributing to the higher premiums. Perhaps the most straightforward reason is that more expensive cars are more expensive to insure and the average price of an new EV is still higher than that for a gas car - although some luxury brands skew those numbers.

Secondly, computerized, high-tech parts, frequently used in EVs, cost more to repair and replace than traditional parts that are produced in mass by budget auto parts manufacturers. But, a lot of it is economies of scale. As EVs become more present on our road, replacement parts, EV specialists, and technicians will also become more popular. Until then, qualified facilities may charge more for their specialized services.

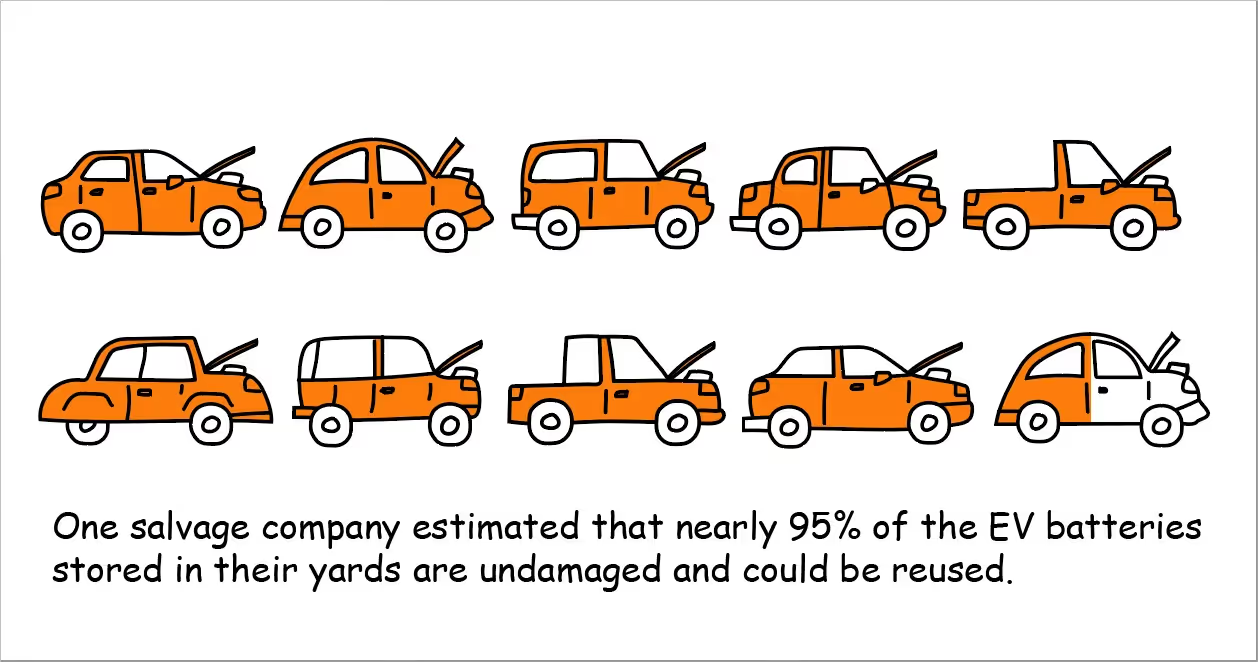

Another issue is at the very heart of EVs: battery packs account for about 50% of an EV’s initial cost and insurance companies tread lightly when it comes to assessing or repairing them after an accident. Even if there is no obvious damage to the battery in an accident, an insurance company doesn’t have a cost effective way to confirm that the battery is still safe. Automakers are also reluctant to share diagnostic data on their batteries with insurers.

This leads to cars that have been in even minor collisions being totaled.

Why? This happens because insurance companies are worried about being liable if a battery they decided was safe has an issue in the future. It is less risk to send the whole car to the scrap yard. One salvage company estimated that nearly 95% of the EV batteries stored in their yards are undamaged and could be reused.

While this is great for specialty shops that can assess and use these packs for battery replacements, it is not an efficient use of resources.

A different California driver had originally switched to Tesla insurance because it was cheaper, only to find two years later, Geico was more competitive with a quote that was a few hundred dollars less.

Still, EV drivers save money

Despite possible higher insurance costs, EV drivers still save money over the life of the vehicle. A recent study found 90% of U.S. households could save money on transportation costs by driving electric vehicles. Much of that savings is in fuel costs, since electricity costs are lower and much more stable than gasoline costs. Savings work out to roughly $1,000 every year. EV drivers can also save 50% on repair and maintenance costs over similar gas vehicles.

Another reason EV drivers may save? Many times, they are going from an older gas car to an EV with lots of safety and driver assist features. In some cases, this means insurance barely changes (or even goes down)!

.avif)

Overall, even when you factor in a higher sticker price and insurance costs of EVs, foregoing a gas powered vehicle and choosing an EV can save drivers $6,000 - $10,000 over the lifetime of the car. If you’re interested in long-term savings, an EV may be the way to go.

Some Insurance Companies Incentivize Green Vehicles

Still, it’s nice to save in the short-term, and fortunately there are several ways to reduce your monthly insurance payment. The number one tip is to shop around. Insurance rates vary by vehicle model, insurance company, and state, so you’ll want to hunt for the best deal. Some insurers offer discounts for electric and hybrid vehicles, though you’ll likely have to ask for a quote before you can find out how much you can save (Note: discounts also vary by vehicle model and state).

- Allstate - EV owners can save more on electric car insurance and get discounts on home chargers, installations and more.

- Farmers Insurance - Those who drive alternative fuel vehicles can save 10%.

- Tesla - Tesla owners in 12 states can also get their insurance through Tesla, which also offers an Autonomous Vehicle Protection Package.

- Travelers - Considered by some to be the best insurer of EVs, Travelers offers 10% off hybrid/electric cars

- USAA - Although only available to military members, veterans, and their families, USAA offers some of the lowest rates across the board.

Many insurance companies offer discounts for paperless billing, safety features, good driving, and even autopay. Since EVs come with many driver assistance features, you may be able to save, especially if you are trading in an older car.

One Tennessee family pays only $10 more a month for a new Mustang Mach-e than for their 2008 Honda Civic - likely because of the safety features in the Mach-e. On the other hand, a driver in the Mid-Atlantic saw premiums more than double when they traded in a 2010 Prius for a 2023 Ioniq 5.

Some insurers have programs to get real-time feedback on your driving habits that can reduce your premiums (assuming you drive safely). Drivers with good driving records can save a lot of money, and you can save with a good credit rating as well. Pay-per-mile plans and bundled plans can also be more affordable. There’s always the option to raise your deductible or pay in an annual lump sum to save even more.